When it comes to securing a mortgage loan, potential homeowners often find themselves faced with a critical decision: should they choose a credit union or a traditional bank as their lender? This choice can significantly impact the interest rates, fees, and overall customer experience throughout the home-buying process. Understanding the differences between these two types of financial institutions is essential for making an informed decision.

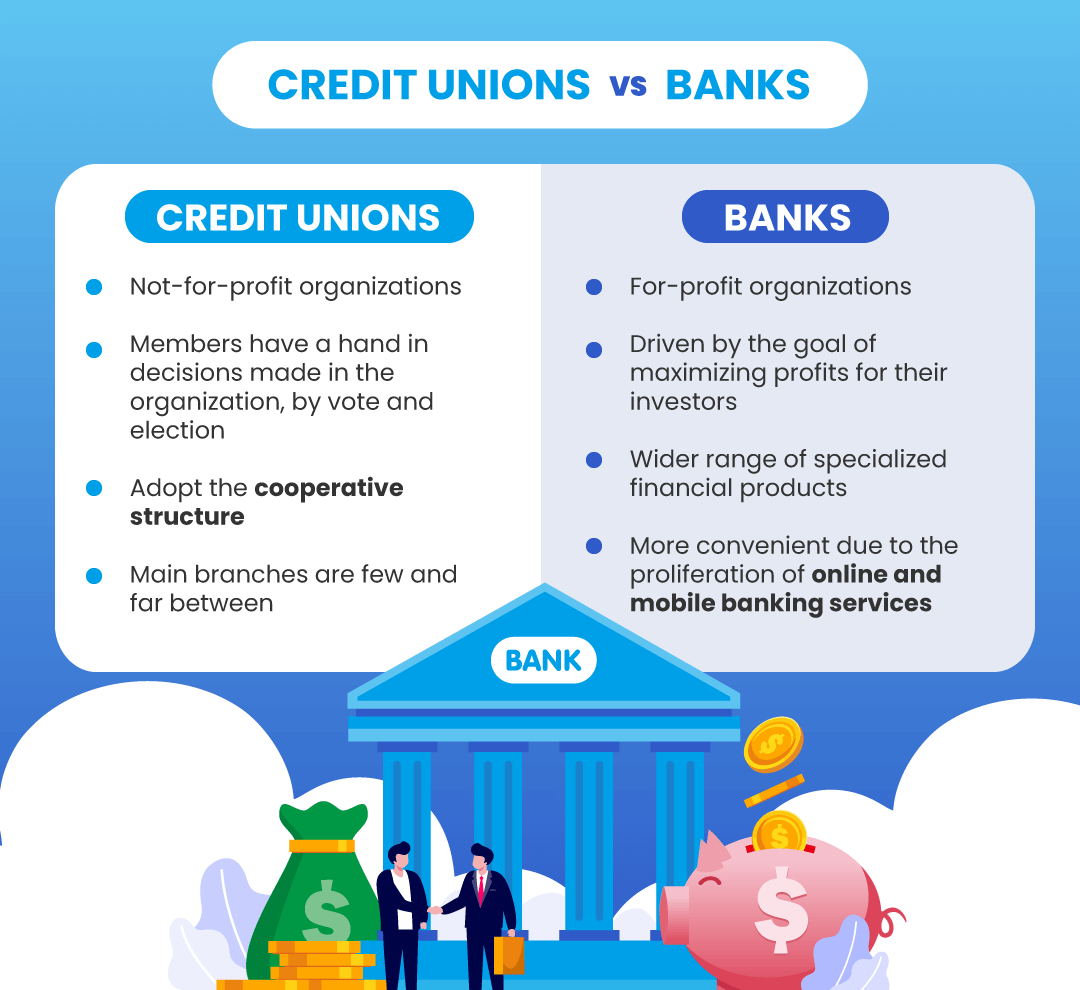

Credit unions and banks operate under different principles and structures, which can lead to variations in the mortgage products they offer. Credit unions are non-profit organizations that prioritize their members' needs, while banks are for-profit entities focused on maximizing shareholder value. This fundamental difference can influence everything from loan terms to customer service, making it crucial for borrowers to weigh their options carefully when considering a mortgage loan from a credit union versus a bank.

In this article, we will explore the key differences between mortgage loans from credit unions and banks, helping you to determine which option may be best suited for your financial situation. From interest rates and fees to customer service and loan flexibility, we will cover all the vital aspects of the mortgage loan credit union vs bank debate. Let’s dive into the details!

What Are the Main Differences Between Credit Unions and Banks?

Understanding the core differences between credit unions and banks can help borrowers make a more informed decision when seeking a mortgage loan. Here are some primary distinctions:

- Ownership: Credit unions are owned by their members, while banks are owned by shareholders.

- Profit Motive: Credit unions operate as non-profits, often passing savings onto their members in the form of lower interest rates and fees, whereas banks aim to generate profits for their shareholders.

- Membership: To obtain a mortgage from a credit union, you must be a member, which may require meeting certain criteria, while banks are open to the general public.

- Customer Service: Credit unions typically provide a more personalized level of service due to their smaller size and member-focused approach, while banks may offer a more standardized experience.

How Do Interest Rates Compare Between Credit Unions and Banks?

One of the most crucial factors to consider when evaluating loan options is the interest rate. Generally, credit unions offer lower interest rates compared to banks. This can be attributed to their non-profit structure, which allows them to pass on savings to their members. However, interest rates can fluctuate based on various factors, including:

- Current market conditions

- Your credit score and financial history

- The type of mortgage loan you are seeking

It is essential to shop around and compare rates from both credit unions and banks to find the best deal for your specific situation.

Are There Differences in Fees and Closing Costs?

In addition to interest rates, borrowers should also consider the fees and closing costs associated with a mortgage loan. Credit unions often have lower fees compared to traditional banks, as they focus on serving their members rather than maximizing profits. However, it’s vital to read the fine print and understand all costs involved in obtaining a mortgage, including:

- Origination fees

- Appraisal fees

- Title insurance

- Closing costs

Different lenders may have varying structures for these fees, so it’s essential to compare the overall costs associated with a mortgage loan credit union vs bank.

What About Customer Service and Support?

Customer service can significantly impact your mortgage experience. Many borrowers report that credit unions provide a more personalized and supportive experience, as they are often smaller institutions that prioritize member relationships. In contrast, larger banks may have more rigid policies and procedures, leading to a more transactional experience.

When choosing between a credit union and a bank, consider the following aspects of customer service:

- Availability of loan officers to answer questions

- Responsiveness to inquiries and concerns

- Willingness to work with borrowers with unique financial situations

Which Offers More Flexible Loan Options?

Another essential consideration when evaluating mortgage loans is the variety of loan options available. Credit unions may offer more flexibility in terms of loan products, especially for members with unique financial situations. Some of the flexible loan options could include:

- FHA loans

- VA loans

- Adjustable-rate mortgages

- First-time homebuyer programs

While banks also offer various loan products, credit unions may be more willing to customize loans to meet individual borrower needs.

How Do Approval Processes Differ Between Credit Unions and Banks?

The approval process for a mortgage loan can vary significantly between credit unions and banks. Credit unions may take a more holistic approach to evaluate a borrower’s financial situation, considering factors beyond just credit scores. This can benefit borrowers with lower credit scores or unique financial circumstances.

On the other hand, banks may have stricter lending standards, focusing primarily on credit scores and debt-to-income ratios. This could make it more challenging for some borrowers to secure a loan through a traditional bank.

What Should You Consider Before Deciding?

Choosing between a mortgage loan credit union vs bank ultimately depends on your financial situation and personal preferences. Here are some factors to consider before making your decision:

- Your credit score and financial history

- Desired loan terms and flexibility

- Importance of personalized customer service

- Willingness to meet membership requirements for credit unions

By weighing these factors carefully, you can make a more informed decision about which lender is right for you.

Conclusion: Which Option is Right for You?

Both credit unions and banks offer unique advantages and disadvantages when it comes to mortgage loans. Credit unions may be the better choice for those seeking lower interest rates, personalized customer service, and flexible loan options. However, banks may provide a broader range of products and easier accessibility for the general public.

Ultimately, it’s essential to shop around, compare rates, and consider your specific financial needs before making a choice. By understanding the mortgage loan credit union vs bank landscape, you can secure the best possible mortgage for your future home.

You Might Also Like

Unveiling The Mystique Of Delphi StadiumUnveiling The Mysteries Of Ikof-7: A Journey Into The Unknown

Understanding Time: How Many Days Is A Million Seconds?

Shemal Dating: Exploring The Unique World Of Connections

Exploring The World Of Hentai Manga Sites: A Guide For Enthusiasts

Article Recommendations

:max_bytes(150000):strip_icc()/dotdash-mortgage-heloc-differences-Final-6e9607c933e9467ba4d676601497a330.jpg)

:max_bytes(150000):strip_icc()/dotdash-loan-officer-vs-mortgage-broker-5214354-Final-4c8f2e5a070a434fafcb2afa1dbe9e1b.jpg)